Celebrations for New Year 2021 were meant to herald a new dawn as the Covid-19 vaccination program was being rolled out and we could finally look forward to life returning to “normal”. Some eleven months later, and while great strides have indeed been made, we can hardly state that normality has returned. The debate on whether vaccinations should be mandatory and the impact of the relaxation of restrictions on those who are not vaccinated, have dominated political discourse both here and internationally. On the world stage, the outgoing Trump presidency at the start of the year saw the storming of the U.S. Capitol building in Washington D.C., an event that shook the foundations of democracy in the United States, while the announcement of a Commission of Inquiry in the BVI at the end of 2020 by the then outgoing Governor, similarly sent shock waves through the local community. But as we approach the end of a turbulent 2021, there are positives to report in the real estate market and the tourist sector is hoping for a strong season as tourist arrivals are poised to ramp up.

COVID-19 Response and Vaccination Programme Roll-Out

In a year when the BVI has been in the spotlight for other reasons, it will be the Government’s handling of the pandemic which will demonstrate how effective they have been both in controlling the spread of the virus and re-opening of the economy to much needed tourism. It must be remembered that the BVI was still in the process of recovery from the 2017 Hurricane Irma which devastated much of the housing and infrastructure in the BVI when the pandemic shut down the economy for a second time.

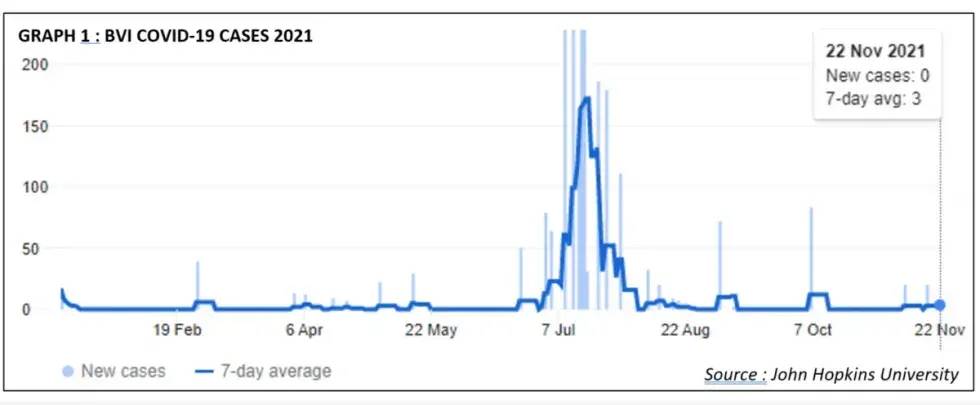

Apart from a spike in cases in the BVI in late June and July when very sadly thirty-seven residents died from COVID-19 (added to the one person who died in 2020), Covid cases in the BVI have generally stayed under control. For many months in 2020 and at the start of 2021, residents could enjoy a relatively relaxed lifestyle within the bounds of the established protocols, with tourists returning to the BVI at the end of 2020, albeit in small numbers. Graph 1 shows the rate of covid-19 infections in the BVI during 2021, reflecting the June/July spike when the Delta variant arrived in the BVI and spread rapidly through the population. Fortunately, a quickly imposed curfew and a responsive population, combined with an effective vaccination programme, brought the spike under control by late August, and by October, active cases were back down to low numbers.

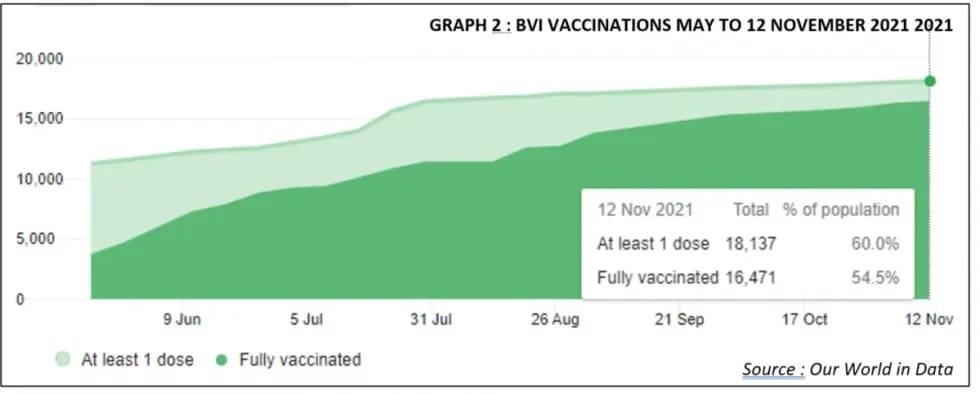

The BVI rolled out its vaccination programme in early 2021, with the first of the AstraZeneca shots being administered in mid-February. Despite Government’s best efforts, including a successful drive-in programme offered around the BVI, the total number of administered vaccinations tapered off from mid-summer with a total of 16,471 persons being fully vaccinated by mid November (Graph 2). According to official statistics, this represents 54.5% of the population being fully vaccinated with 18,137 having received their first dose bringing the total to 60.0% of the population by 12 November. In the summer of 2021, the Government also arranged for anyone in the BVI to travel to the USVI to receive the Pfizer vaccination as some remained skeptical about possible side effects of the AstraZeneca vaccine. It should be noted, however, that the official Government population statistics are based on the 2010 population census with a total population of 28,054. Since then, many people have left the BVI following the impacts of Hurricane Irma and there have been further repatriations of workers following the slowdown in the economy as a result of the pandemic. The Government’s current population estimate, with no new census having taken place in 2020, is 30,253.

The Government’s aim is to reach “herd immunity” with 75% of the population being vaccinated which requires a further 6,000 people to be fully vaccinated, with a target of 80% of the population being vaccinated to be effective against variants (Graphic 1). Given the lack of progress in increasing the number of persons being vaccinated since the summer, it seems that the BVI will remain at between 55% and 65% of the population being fully vaccinated unless additional factors come in to play. It is expected that boosters will be provided for vulnerable persons and people from mid December.

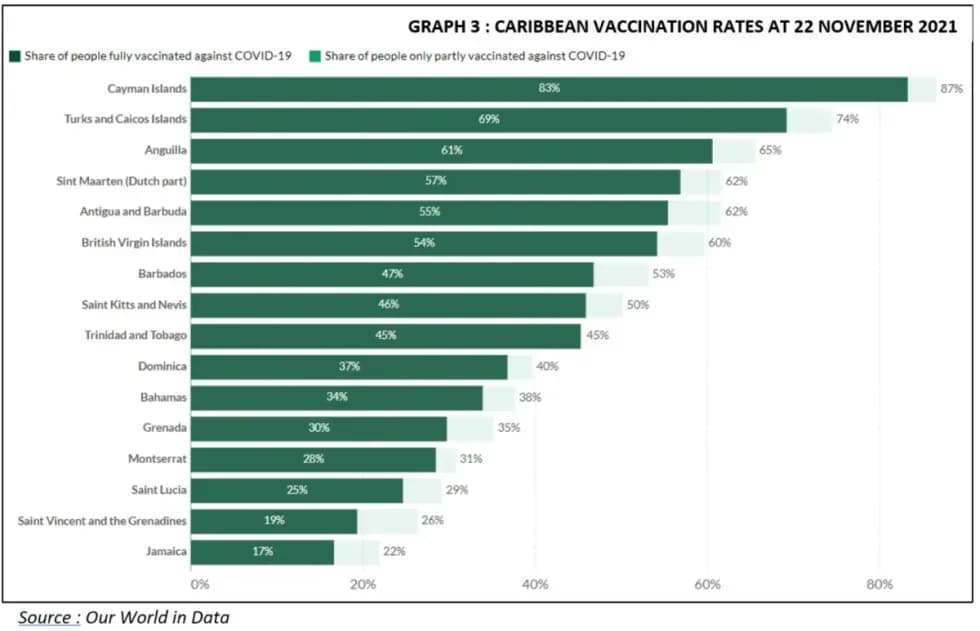

Despite the number of persons being vaccinated leveling off, the BVI is ahead of the independent Caribbean Islands who are struggling to vaccinate their populations as shown in Graph 3. The British Overseas Territory of Cayman Islands has exceeded 80% of the population being fully vaccinated and Turks & Caicos Islands is at 69% while Anguilla is over 60%, demonstrating how the support for vaccinations from the UK has helped the vaccination programmes in these Territories.

The Government has to steer the fine line between keeping the economy running, encouraging tourism to return to the BVI and protecting those who remain determined not to be vaccinated. The question of whether to mandate vaccinations on all, or some, sectors of the population have not yet had to be addressed in the BVI. Attempts to do this in other countries have been met with opposition and hostility

Economy and Tourism

As 2021 rolls to an end, the climate crisis is once again front page, ahead of the pandemic that took centre stage in 2020. With the Global Climate Change Summit (COP26) in Glasgow concluded, the world’s nations are under the spotlight to finally implement strategies to reduce carbon emissions. Focus is also on inequality, not just in relation to the impact of climate change on poorer nations, but also on how the vaccine rollout programme has been first-world-centric. At the G20 summit preceding COP26, agreement was reached on setting a minimum corporation tax rate of 15%, a move to prevent multi-nationals from diverting profits through low tax jurisdictions.

Preceded by the Paris Agreement in 2015, which targeted keeping temperatures to 1.5°C above pre-industrial levels, and well within 2°C, and reaching “net zero” greenhouse gas emissions between 2050 and 2100, COP26 has reset targets being adopted. In the end, COP26 ended with an “agreement to agree” with nations meeting again next year to pledge to deeper emissions cuts. The summit was overshadowed by China and India watering down language on the phasing out of coal to “phasing down”, much to the dismay of many smaller nations already impacted by climate change. Poorer nations are holding the wealthier nations to account, both in terms of meeting their commitment to the Paris Agreement and in particular to Climate Financing, whereby the wealthier nations pledge $100bn annually to support developing nations meet their climate goals. Scientists are in no doubt that the stakes are high with current pledges, if fulfilled, limiting temperature rises to around 2.4°C, still well above the intended target of 1.5°C.

Aside from the medical impacts of Covid-19, the extended lockdowns experienced throughout all economies have played havoc with supply chains, the demand for labour and Government debt as stimulus packages have increased Government borrowing to levels not seen since the Second World War. As economies have reopened, there has been increased labour demand as firms seek to ramp up supply of goods however supply chain issues have impacted economies around the world, in turn leading to increasing prices and the return of inflation which reached 5.2% in the US in September. With poor third quarter growth in the US, as the drag of increased Covid cases caused by the Delta variant took hold, combined with a slow-down in vaccinations, the higher than expected inflation has sent ripple effects through the US economy and beyond. While most economists believe that the slow-down is temporary and the Federal Reserve presently has no plans to increase interest rates to counter the impact of inflation, the emergence of the new Omicron variant could change the response if economies are once again shut down through new quarantine requirements and restrictions on travel.

Concerns about inflation, reduced economic stimulus and supply chain woes have dampened stock markets that had experienced significant growth earlier in the year and the announcement of the Omicron mutation led to market jitters at the end of November indicating the continued impact of the pandemic on the economy. Fund managers are cautious about prospects, with inflationary risks the main area of concern, leading to de-risking of investment portfolios. However, more fund managers are taking stock of changing trends regarding ESG (environmental, social and governance) concerns as investors take heed of messages from scientists and activists on climate change and equality, and Governments on regulation.

Following a projected upturn in the US economy in the fourth quarter, the economic outlook for 2022 is for a slow-down in growth while inflation rates remain uncertain. The question of how the Federal Reserve will respond to stagflation, either through raising interest rates or further stimulus of the economy, will determine how the economy responds next year. The fragile balance of power in the Senate stalled President’s Biden’s plans for his infrastructure bill, although it was finally passed in a reduced format in early November, and he arrived at COP26 without his climate change plan approved. The recent avoidance of a government shutdown indicates the delicate balance of power that is being played out in the States. The election for the governorship in Virginia resulted in a shock win for the Republicans, indicating the lack of popularity of the Biden administration (a rating of just 43% by early November) and reflecting how the passage of Biden’s agenda had become mired in political wrangling combined with the chaotic withdrawal from Afghanistan in the summer. Interestingly, the newly elected Republican challenger in Virginia managed to appeal to the Trump base as well as moderate Democrats, without inviting the support of Trump during campaigning. How the US economy performs next year, the confidence in equity markets and the general outlook of investors will play a significant part in determining the economic outlook in the BVI and the wider Caribbean.

The BVI’s twin pillars, financial services and tourism, have both suffered impacts in recent years which have in turn impacted funding for central government. Financial services have come under pressure internationally, particularly after the 2008 financial crisis, from Governments seeking to stabilize their economies and preventing multi-nationals avoiding paying tax by establishing bases in low tax jurisdictions which has culminated in the G20 agreement to a minimum 15% corporation tax rate.

The regular leak of information from “offshore” financial jurisdictions (Panama Papers 2016; Paradise Papers 2017 and Pandora Papers 2021) has provided fuel to the fire to impose good governance and transparency on jurisdictions involved in financial services. The UK has been pressing for the imposition of public registers in the BVI (and other jurisdictions), a move the BVI has said it is willing to commit to by 2023 provided all jurisdictions have the same requirements as the BVI. In announcing the decision to move to public registers in October 2020, Premier Fahie stated “The format must be in line with international standards and best practices as they develop globally and, at least, as implemented by EU member states. In advancing this commitment, we will be informed at all times by global best practice at the time within a timeframe that we consider deliverable.”

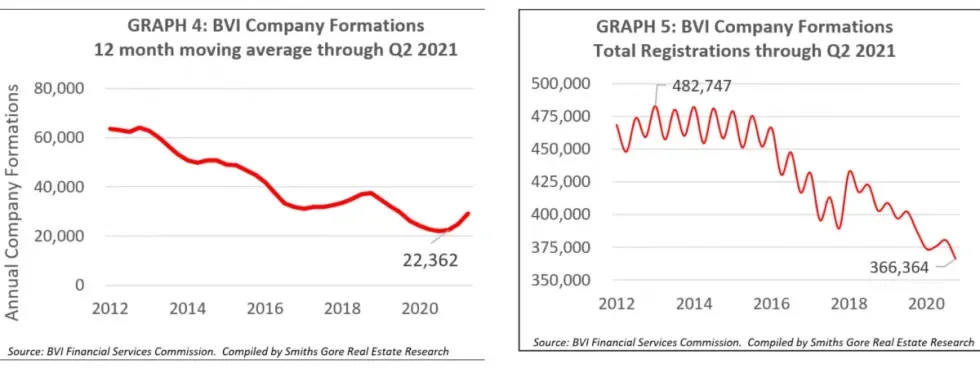

The foundation of financial services in the BVI is the formation of companies which has experienced a decline in recent years. Graph 4 shows the 12-month moving average for company formations from 2012 which demonstrates the general downward trend, as does the total registrations shown in Graph 5 which has fallen by 116,383 registered companies between Q1 2013 and Q2 2021, a fall of 24% over the period.

The significant declines in company formations in 2019 and 2020, following modest increases in 2017 and 2018, is concerning for the industry and more particularly for Government where 60% of revenues are derived from the financial service sector. Revenues from the sector fell by approximately US$30M, or 3% of GDP, in 2019 with a similar fall in revenue in 2020, accounting for 52.68% of total revenues in 2020 compared to 59.31% in 2018. This placed the BVI in a deficit in 2020 of approximately $30M with revenues totaling approximately $360M against expenditures of $390M. On 11 November 2021, the Government announced their 2022 budget of $397.17M with the Ministry of Finance predicting revenues of $356.7M of which $323.2M will be derived from taxes and $33.5M from other sources. It is not yet clear how the budget shortfall will be addressed.

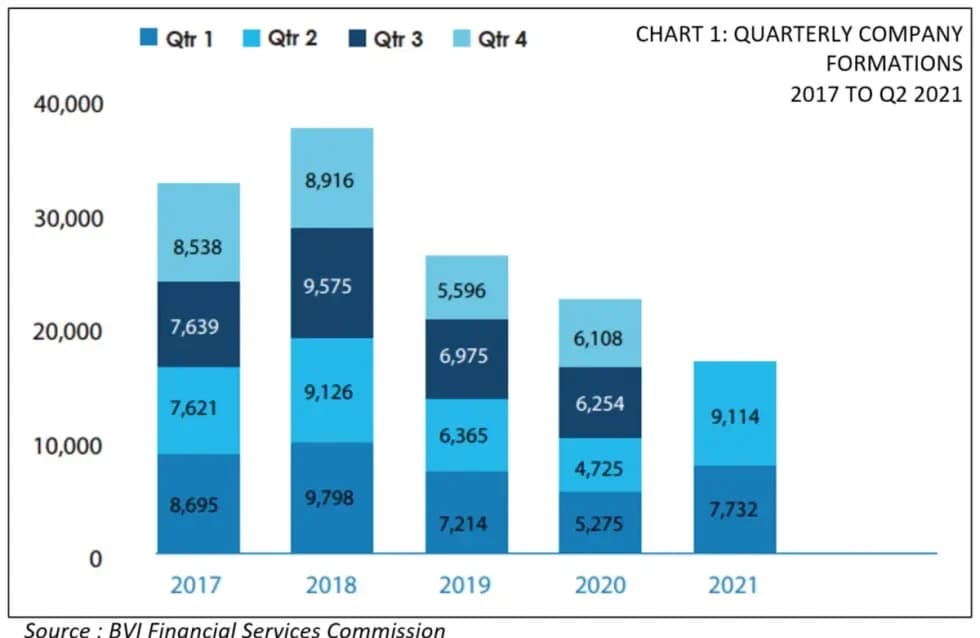

There is some light on the horizon as both Q1 and Q2 2021 showed significant increases in company formations compared to 2019 and 2020. Chart 1, prepared by the Financial Services Commission, shows company formations by quarter between 2017 and 2021, with the first six months of 2021 indicating that the half year formations were similar to 2017.

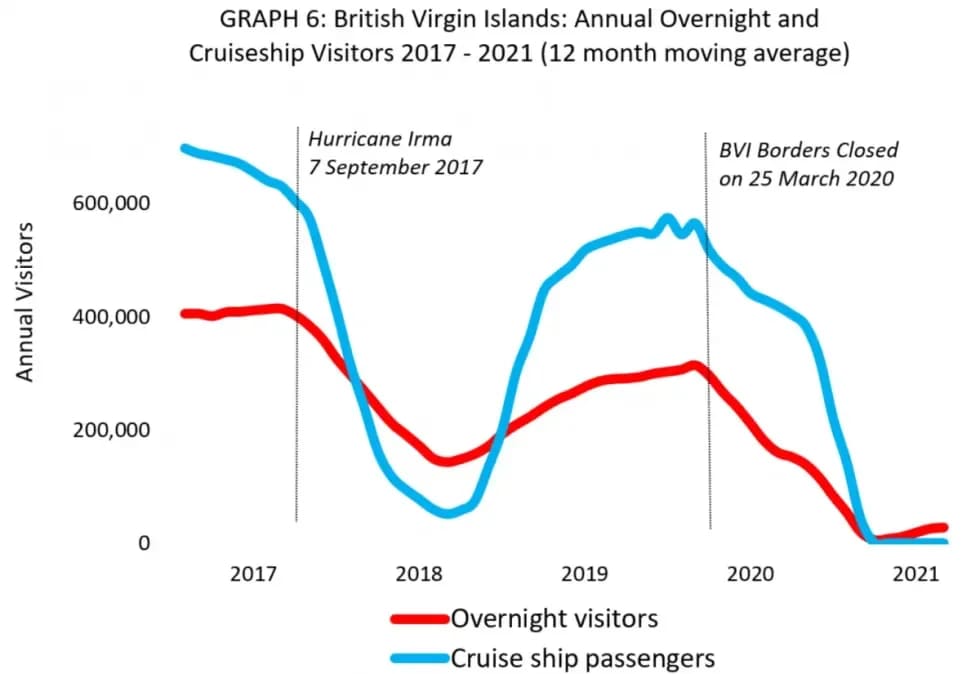

While the performance of the financial services sector is a long-term concern, the impact of first Hurricane Irma and then the pandemic on the tourism sector, the second pillar of the economy, has also been significant, both in terms of impact on government revenues and, as importantly, the businesses and employees offering services in the tourism sector. Graph 6 shows the impact of these events on tourist arrivals to the BVI, both overnight and cruise ship passengers. Prior to Irma, overnight tourists, which include hotel, villa and yacht charter guests, averaged around 400,000 arrivals each year, with 50% of those arrivals from the yachting industry. Following Hurricane Irma, the yachting industry sustained tourism in the BVI for many months before the hotels and villas were repaired and reopened again to visitors. The pandemic impacted hotel/villa and yachting industries alike and businesses have struggled to remain solvent through the now nearly two years that the pandemic has impacted the BVI.

Prior to the pandemic, in 2016, cruise ship arrivals had increased to 700,000 plus arrivals a year, mainly as a result of the upgrading of the cruise ship dock to accept the larger cruise ships which by then made up the majority of the cruise ship fleet. Cruise ship arrivals then halted for a better part of a year after Hurricane Irma while the cruise ship companies waited for the islands to be ready to accept their passengers back. This was in contrast with the many overnight visitors from hotels, villas and charter yachts, who were keen to return to the BVI as soon as it was safe and practical to do so in order to support the economy, even though the BVI was still in the process of rebuilding.

The winter of 2019/20 was the first high season following Irma to see visitors return to the BVI in larger numbers as more hotels and villas reopened. The yacht charter industry had also rebuilt the charter fleets and were likewise expecting a good season as was the cruiseship sector. All this optimism was cut short in late March 2020 when the pandemic lockdown was announced, and tourism was halted over-night.

The government established strict travel protocols during 2020 for nationals and residents returning to the BVI, although it was some time before work permit holders were permitted to return to the BVI. An online travel gateway was established towards the end of 2020 as the tourism sector became anxious to see tourists return to the BVI, with tourists being permitted to return on 1 December 2020. The application process and quarantine requirements on arrival evolved over the course of 2021, particularly as persons became double vaccinated. Eventually, with effect from 1 October 2021, all persons who were double vaccinated were permitted to enter without having to complete the gateway application but with the proviso of taking a rapid flow test on arrival.

While hotels, villas and charter companies are reporting strong bookings for the high season as travel restrictions ease and more people are double vaccinated, there have been issues for many companies in preparing for more guests, particularly with delays in re-employing labour that had previously been severed. The yacht charter industry has also had turbulent times as the Shipping Registry and BVI Customs Department are now enforcing regulations just before high season that were first enacted over twenty years ago. The regulations call for all commercial vessels in the BVI to conform to certain regulations with the Shipping Registry giving the various charter companies about two weeks to comply, which involves also having each boat surveyed.

While the charter industry is not opposing the enforcement of regulations, the timing and lack of notice has created issues for previously booked charters resulting in many of the foreign owned vessels and high-end crewed charter vessels relocating away from the BVI. Regulations are also impacting mega yachts and foreign-owned vessels that have scheduled visits to the BVI during the season due to an increase in documentation required in order to carry out charters, resulting in some cancellations.

Development in the BVI

Four years following Hurricane Irma, two of the BVI’s iconic watering holes in North Sound, Saba Rock and Bitter End Yacht Club, have been rebuilt and are re-opening for business which will provide a tremendous boost for tourism in North Sound which has otherwise lacked bars and restaurants to attract tourists. Saba Rock, which was sold following Hurricane Irma, was completely rebuilt and reopened for business on 16 October. Sitting between North Sound and Eustatia Sound, Saba Rock Resort provides a classic bar and restaurant location for waterborne guests along with nine guest rooms and suites. While similar to the resort that existed prior to Irma, the redesigned property incorporates significant structural changes both in terms of upgrades to cope with future climate events, and also with the interior design and layout.

Bitter End Yacht Club has an established following in the yachting fraternity, created over the many decades that the resort has been operating. After the original resort was leveled by Hurricane Irma, the owners started plans for phase one of what they referred to as “BEYC 2.0” with a nautical village offering a range of facilities including The Clubhouse, with a multi-concept seaside restaurant and beach bar, the Bitter End Market and Reeftique plus two self-catering marina lofts, with more to follow in further phases. Centred around a village plaza, the development has echoes of the past, with the Quarterdeck building and generous use of timber throughout, but draws on modern design and contemporary finishes to complete a modern waterfront mixed-use complex. BEYC 2.0 is expected to re-open towards the end of 2021.

Oil Nut Bay has now been under development for twelve years, establishing itself as one of the leading residential resorts with over $600M of owner investment to date. In addition to the established central facilities, which include Beach Club, fitness centre, tennis and pickleball courts, nature centre, kids’ Nut House and two heli-pads, recent development has also focused on the marina village which includes a 93-berth marina plus the over-water Nova restaurant with accompanying retail and leisure outlets including a day-spa which is due to open in 2022. With around $100M in new construction each year, there are now fifty villas completed or under construction with four new villas introduced into the rental programme this year and a further six villas being added over the next year. Guest experiences at the Beach Club now include the Pavilion, an exclusive area where homeowners and in-house guests can curate the menu and enjoy the private hot tub and fire-pit.

The Marina Villas, comprising two, three and four bedroom rental ready units, will be completed in 2022 and developer, David V. Johnson, recently announced the release of newly available homesites on Pajeros Point, the most easterly point in the BVI. Lots at The Peninsula and Wild Side range in price from $3.95M to $25M for the 10.79 acre Point Estate. The development is also about to commence building their zero set-back Ocean Villas, two three-bedroom spec homes and a six-bedroom villa situated on a white sand beach. Oil Nut Bay continues to be a major source of employment and revenue for the BVI and will also provide opportunities for construction and further development for many years to come.

Scrub Island is an established resort with a residential component which is enhancing its green credentials. A solar array, capable of providing over 50% of the resort’s power, has been installed within the past year and a chef’s garden created to improve sustainability through the provision of their own herbs and seasonal produce. Landscaping throughout the resort has been enhanced to balance the built environment with nature using indigenous plants and natural materials. Scrub Island will be completing two new villas in 2022, each offering three-bedroom suites and spacious living areas with the first due for completion in January.

Scrub Island have also announced that they will be taking over the operation of the adjacent Marina Cay, having signed a long-term lease with the owner towards the end of 2021. This iconic island, for many years home to a Pussers outlet, is one of the key stop overs for yachts cruising around the BVI. With thirty moorings available, Scrub Island intend to bring back the island’s nostalgic past, once again providing visitors with an anchorage and landside facilities.

Nanny Cay Resort and Marina announced the opening of their Seaview Wing of new hotel rooms at the end of October 2021 which are due to open to guests from 1 December. Comprising Superior rooms on the first and second levels and Premium rooms on the third level, each room offers 400 sq ft of interior space with a balcony overlooking the Sir Francis Drake Channel. The hotel at Nanny Cay also has 34 existing rooms in the garden wings with the standard rooms on level one being refurbished while the deluxe rooms on the upper level have been completely rebuilt. Once the Seaview Wing is completed, the hotel will have a total of 52 keys in addition to two and three bedroom town houses which are also offered for rent through the hotel.

Nanny Cay has also been addressing the operation of the marina, focusing on the availability of slips to over-night renters and charter companies to maximize the number of guests who will be utilizing the facilities at Nanny Cay. With Navigare and Waypoint yacht charter companies both commencing operations at the marina this high season, Nanny Cay will be catering to many more guests than in prior years, particularly with the charter companies predicting a busy season. To this end, Nanny Cay have reorganized some of their guest services and will be introducing “Omar’s’” to the Nanny Cay food and beverage options while the Spa will relocate to a larger unit providing improved services to guests.

On Tortola, there are a number of significant commercial development projects underway which are being developed by BV Islanders. One Mart is expanding its operation in East End with the construction of a new 12,000 sq ft store, and more planned elsewhere on Tortola. JOMA Properties, one of the leading locally owned property development companies in the BVI, have launched their Road Harbour Marina project, a mixed used development which is planned to include a 65-room boutique hotel in addition to commercial and residential space plus the revamping of the existing marina services. In Road Town, the six storey 26,000 sq ft Lunar Tower occupying a prime location on Waterfront Drive, is due for completion in Q1 2022, offering prime office space and retail units.

Investment Act and Business License Act

The majority of the resort development in the BVI in recent years has been focused on the expansion of existing facilities with just a small number of greenfield sites being developed. Scrub Island, Oil Nut Bay and YCCS Yacht Club and Marina are three examples of new developments and Moskito Island is essentially a ground up re-development of an older resort. This is unusual in the Caribbean where most islands have benefitted from new development over the years. Development starts during 2021 in many islands have signaled a revival of the resort sector since the economic crisis in 2008 ended the last development boom between 2004 to 2007.

That the BVI has not seen many new build developments is due to a complex number of reasons with indirect air access through regional hubs often being mentioned as a prime reason for the lack of development in the BVI. However, many developers and investors will also point to the difficulties associated with investing in the BVI, with delays in approval processes increasing the development risk compared to other islands.

The Government is introducing two new acts in an attempt to address many of the concerns expressed by investors with investing in the BVI. The Virgin Islands Investment Act 2021 was passed in August and replaces the Pioneer Services and Enterprises Act, the Hotel Aid Act and the Encouragement of Industries Act. The Business Licensing Act, which replaces the Business, Professions and Trade Licences Act, is currently passing through the House of Assembly and has received its first reading.

By introducing these two acts, the Government is aiming to enhance development on the BVI through both domestic and international investment, while at the same time introducing legislation which makes it harder for foreign entities to front their ownership of a business through a local (Belonger) entity. Central to both acts is the introduction of the Virgin Islands Trade Commission which has been established under the Virgin Islands Trade Commissions Act. The Commission will be tasked with considering investment proposals and approving investment plans as well as promoting investment in the BVI. It will also maintain a register of both domestic and international investors and their investments which exceed a certain (as yet undefined) threshold. The same Trade Commission will also be responsible for reviewing and approving applications for business licences under the Business Licensing Act. The two acts introduce some fundamental changes to the process of investing in the BVI, particularly for foreign investors. The principal difference is that prior to applying for a business licence, a foreign investor first has to apply for, and be granted, a certificate of approval under the Investment Act. The application will be considered against a range of criteria which include the contribution the proposed investment will make to the BVI with respect to employment and training of the workforce, the procurement of goods and services domestically and the impact on the environment. Additional considerations apply for foreign investment, including the creation of a joint venture with a Belonger, employment of Belongers, the transfer of technology, skills and management expertise and the promotion of research, development and innovation.

The Investment Act includes the ability for the Minister to facilitate the granting of visas and resident permits to foreign investors, their immediate families and foreign personnel including either the approval for the long-term engagement of foreign personnel or the temporary engagement for a prescribed period. The Act reserves certain sectors of the economy (yet to be defined) for Belongers or entities which are majority owned by Belongers and foreign investors may be required to enter into a performance agreement with the Commission which in turn will establish a client service facility to facilitate the application and approval processes for required permits and licenses. The Act also establishes the National Economic Investment Fund which investors with qualifying investments will be required to contribute to. The fund will be used for infrastructure development, environmental protection, development and social programmes. The Act does not specify when a contribution shall be made or the amount of the contribution.

The schedule to the Investment Act outlines the types of investment incentives available, projects eligible for investment incentives and areas for investment incentives. The Act does not set out in detail how these will be administered, except that regulations will be established to give effect to the provisions of the Act.

The Investment Act provides two schemes for foreign investors. The first, the Invest and Stay incentive, is not described in detail except that the minimum investment to qualify for this scheme is $5.0M and that 60% of all employees should be Belongers. The Invest and Stay incentive offers investors a two year entry permit that can be extended for further periods of two years while the investor owns the business. The second scheme is the residency by investment scheme. This scheme is administered by a Residence by Investment Unit which reports to a Residence by Investment committee. Applicants for this scheme have to apply through an approved agent, who has to be a Belonger. Details for this scheme have yet to be developed, including what level of investment is required. An approved investor is not permitted to apply for Belongership until after a period of twenty years has lapsed since the date of application for residency.

The Investment Act gives the Commission rights of expropriation, subject to the payment of compensation, which includes “an asset, a property right or any other right of an investor….”provided the expropriation is “taken in the public interest”. A foreign investor can transfer funds for the investment into and out of the Territory, subject to the laws of the Territory, but “the Minister, on the advice of the Commission, may delay or prevent a transfer …..” in certain prescribed circumstances such as insolvency, to protect creditors or to ensure compliance with judgements or tax obligations. The Act also states that “in exceptional circumstances, to prevent movements of capital that causes or threatens to cause serious difficulties for macroeconomic management of the economy.”

A foreign investor is required to pay the initial capital required (not defined in the Act) for the investment before the Commission “shall issue a certificate of approval of investment that allows the foreign investor to register with the Commission and commence with the investment.” However, it is only once the certificate of approval has been granted that the foreign investor can then apply for a business licence. The Business Licensing Act requires that all persons engaging in business activity in the BVI shall first obtain a business licence, which includes certain businesses which are currently licensed under separate legislation such as the Securities and Investment Business Act 2010. The cost of business licenses face a substantial annual increase, particularly for foreign investors, with the cost of licenses ranging between $150 to $1,500 for Belongers and $1,500 to $15,000 for foreign investors.

For Belongers, the process of applying for a business licence is not dissimilar to the process currently in place for trade licenses with the exception of the cost of the licenses, which will increase. For foreign investors, applications have to be accompanied by a certificate of approval for investment and an investment business profile along with personal and business references, police report and other required documents including evidence of experience in the industry being applied for. Applications for businesses also need to provide evidence that the business is majority owned by a Belonger. There seems to be some debate about this point as during a public meeting on the two acts held by Government, the representative making the presentation stated that a foreign investor will be entitled to apply for a business licence through a company which was not majority owned by a Belonger. The discrepancy was pointed out during the meeting so the final version of the act may clarify this point.

Renewal of business licenses require each business to make an application for renewal accompanied by certain documents which include a certificate of good standing, evidence that all payroll contributions have been made, registers of shareholders and directors, any licence or permit required under any other law to engage in the business and the renewal application fee. The Commission will consider the same requirements for a renewal of a license as it did when originally granting a license, namely the previous conduct of the business and the persons holding an interest, whether the business or proposed business activity has been reserved for Belongers, the efforts made by the company to obtain Belonger participation in their business, the necessity to limit the number of businesses operating within a particular sector and the socio-economic impact of the proposed business activity to the economy of the BVI.

Schedule 1 of the Business Licensing Act has three parts : Part A sets out business activity annual fees; Part B sets out reserved business activities annual fees and Part C joint venture business activities annual fees. The Act states that business activities specified in Part B are reserved for Belongers and a non-Belonger may not engage in any business specified in Part B unless authorized to do so by the Commission. The Act specifies that this restriction does not apply to non-Belongers already licensed for a restricted activity prior to the commencement of the Act. Part C relates to business activities where a non-Belonger may enter into a joint venture with a Belonger. The Act also states that “the Minister shall prescribe the percentage of the issued share capital” when deciding what constitutes the majority Belonger ownership in a company.

The acts referred to above set out a radically new framework for the Government to engage with investors, both domestic and foreign, although the Investment Act does focus particularly on the nature of foreign investment in the BVI. Both acts encourage the participation of Belonger investment in foreign owned companies and actively promote joint ventures, although in a transparent manner to avoid the issues of “fronting” which, although illegal under existing legislation, has been perceived to happen too often. There are many questions still to be answered relating to the acts, and particularly the Investment Act. The threshold of investment which will determine qualification for registration as an investor has not been determined and presumably will separate the types of investment that the Act is intended to capture. While “assets that are of a personal nature, unrelated to any business activity” are not captured by the Act, and could therefore presumably include investment in residential property for personal use, the question arises whether foreign investors wishing to acquire a residential property with the intention of renting will be captured by the Act if the level of investment exceeds the yet unknown threshold.

UK and BVI Relations

The BVI has been in the spotlight this past year with a Commission of Inquiry (COI) established by former Governor Augustus Jaspert just prior to his departure at the end of 2020. Sir Gary Hickinbottom, a senior UK judge, was appointed as the sole Commissioner and the terms of reference as set out on the Commission’s website are “to establish whether there is evidence of corruption, abuse of office or other serious dishonesty that has taken place in public office in recent years, and if so what conditions allowed this to happen. This will ensure that BVI’s governance is working in a fair and transparent manner for the people of BVI. The Commissioner will report his findings and recommendations to the Governor. The Commission of Inquiry is not a court, therefore it will not make findings of criminality.”

The Commission, convened on 18 January 2021, commenced private hearings in the week commencing 3 May 2021 and public hearings in early June. In the interests of transparency, public hearings were shown live on a dedicated You Tube channel, allowing the public to follow the Inquiry firsthand. The COI covered a range of topics during the public hearings including the Government’s handling of the pandemic stimulus packages, statutory boards, Crown lands, the Auditor General’s reports (and by extension the various projects the reports were reviewing) and a range of other topics. Former Governor Augustus Jaspert and current Governor John Rankin also both appeared before the COI. The final public hearing was held on 17 November 2021, with the cross examination of the present Governor at the request of the BVI Ministers. The Commissioner is expected to report to the Governor on his findings in early 2022.

The Commission of Inquiry has been momentous for the people of the BVI, exposing the inner workings of Government, and has divided the populace between those who view the COI as an imposition by a colonial power and those who hope the COI will lead to change in how the BVI Government operates. Whatever beliefs are held, the COI should bring about change, not just for the BVI but also for the UK in the way it administers the Overseas Territories.

Outside of the COI, the BVI is still undertaking a review of the constitution which was last updated in 2007. In February 2021, the Government approved funds to establish the Constitution Review Commission amid calls for the BVI to have greater control over its internal affairs. Some of these issues have been highlighted in the COI, but in August, the UN reaffirmed the BVI’s right to self-determination at the United Nations (UN) Committee of 24’s (C-24) regional seminar on decolonization held in Dominica. The Deputy Premier, Dr Natalio Wheatley, expressed concerns at the seminar that the UK would use the findings of the COI to take away the BVI’s autonomy. Dr Wheatley stated after the seminar, “The UN via the C-24 has again reaffirmed the right of the people of the British Virgin Islands to self-determination and for self-governance in the Territory to be upheld. They have clearly called on the Administering Power, the United Kingdom (UK), to respect the UN Charter and international law which covers the special rights of the BVI and those societies on the UN list of Territories yet to be completely decolonized. This includes the BVI’s current constitutional position and plans for Constitutional Review.”

Relations between the BVI and the UK have unquestionably been strained with both the former Governor and the Premier each pointing to reasons for the breakdown in their interaction which were highlighted during the COI hearings. Neither the UK nor the BVI will wish for this situation to continue, although the outcome of the COI could determine the next steps with regard to progress with the constitutional review.

BVI Real Estate Market Review

Despite the many issues that have impacted the BVI since 2017, the real estate market has generally proven to be resilient. Bouncing back after Hurricane Irma in 2017, the market was driven by local investors acquiring damaged homes from mainly foreign investors who sought to exit their investments rather than face rebuilding in uncertain times. By late 2019, with many homes repaired and the first high season where foreign investors could properly visit the BVI after the hurricane, there was a return to more normal market conditions. However, this was quickly brought to an end in late March 2020 as the outfall from pandemic swept through Europe and the Americas, closing borders and stopping visitors from entering the BVI.

Far from the real estate market slowing down, the local (Belonger) market continued to invest in property during 2020, buoyed by the stamp duty exemption for Belonger purchasers which was introduced in 2020 and then extended to the end of 2021. 100% loans on land were also offered to Belonger purchasers by the National Bank, further encouraging investments in land. While foreign investors were limited in making inspections due to restrictions on travel, new ways of presenting property through virtual tours kept the overseas market alive until borders could re-open and inspections could take place. Some sales to overseas investors even occurred without inspections having taken place, relying on virtual tours and video presentations, but these were the exception.

2021 has witnessed a real estate boom in North America where agents have reported a record number of sales fueled by pent-up demand following the reopening of economies. Many islands in the Caribbean have seen a similar boom, with investors seeking second homes, for personal use or investment, which has been reflected in record sales in many jurisdictions. While the real estate market in the BVI has improved both in terms of levels of interest and number of sales, the market remains slower than in other parts of the Caribbean. The data shows that the market is dominated by sales to Belongers rather than an increase in interest from foreign investors although this may change once sales to foreign investors, which commenced in 2021, start to close towards the end of the year or early 2022.

There are a number of reasons why the BVI real estate market may lag behind other Caribbean destinations, with airlift, Government regulations and pricing all playing a part. Ultimately, property in the BVI takes time to sell, unless competitively priced, and for the past fifteen years, the supply of houses has been greater than demand. The exemption on stamp duty for Belonger purchasers has, as noted above, fueled an increased number of sales with land sales in particular growing considerably in late 2020 and early 2021, with demand for land outstripping supply for small to medium sized lots.

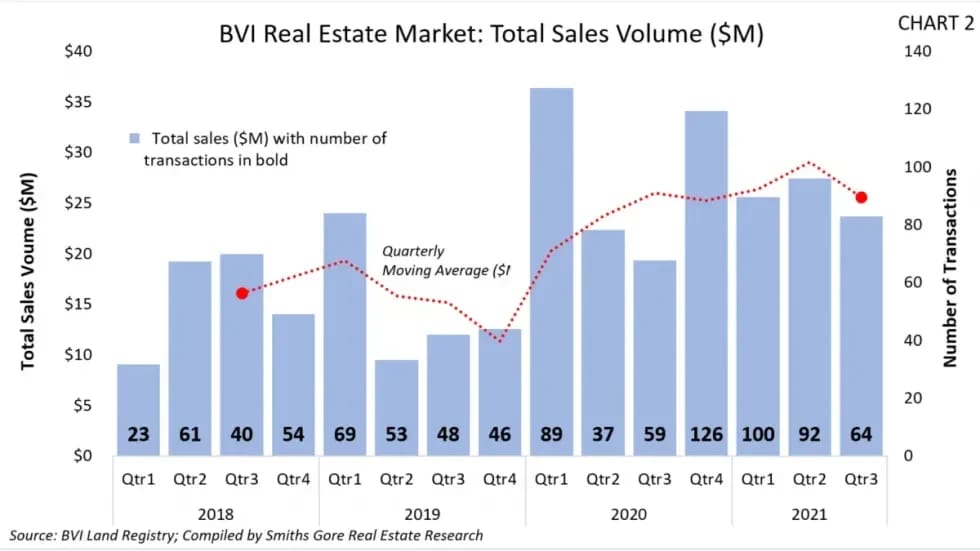

The post Hurricane Irma real estate market has been active particularly amongst local investors. The following charts and graphs show how the real estate market has changed over time as Belongers have replaced foreigners as the primary investors in real estate in the BVI. First, with Chart 2 we look at total property sales for all categories (land, residential homes and commercial property) by quarter since 2018. This shows the increase in sales in 2020 which started before the pandemic lockdown began (late March 2020) but was then sustained for the remainder of 2020 and 2021 through the stamp duty waiver for Belonger purchasers which came into effect in July 2020 (with exemptions back dated to May 2020). The cost to Government of the stamp duty waiver is estimated at $4.35M based on sales to Belongers between May 2020 and September 2021.

The total volume of sales doubled from $58M in 2018 to $112M in 2020. 2021 is also on course to record significant total sales with $74M in completed sales through to the end of September 2021. With the stamp duty exemption ending in December 2021, it is expected that there will be a number of Belonger purchasers looking to push sales though prior to the end of the year.

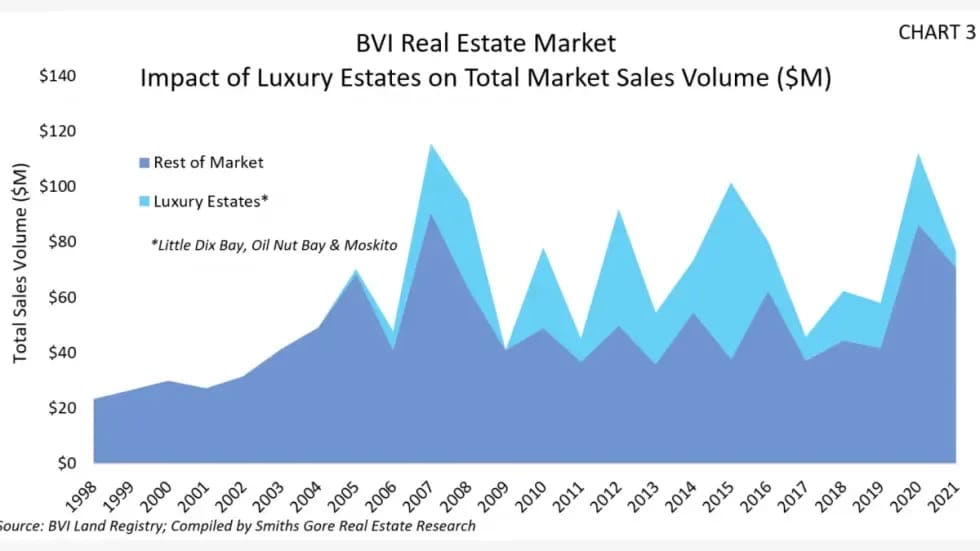

The impact of foreign investment on the property market in the BVI is significant, not only in terms of stamp duty income to the BVI Government, as foreign investors pay a rate of stamp duty at 12% compared to Belonger investors at 4%, but also through the rentals that follow where foreign owners have been granted consent to rent under their landholding licence or through a resort development. The villa rental market in the BVI provides significant land-based accommodation which in turn generates hotel accommodation tax for the Government plus income for local businesses including car rental firms, restaurants, spa and health providers, provisioners etc. Chart 3 demonstrates the impact on total sales volume of property sales at Oil Nut Bay, Moskito Island and Little Dix Bay, the three prominent resort developments in the BVI with residential components. The chart shows how sales initially commenced at Little Dix Bay in 2005 with sales at the resort peaking in 2007-08. Sales at Oil Nut Bay and Moskito Island commenced in 2010 and peaked in 2015/16. There followed a decline in sales in 2017/18 following Hurricane Irma before sales picked up again in 2019 and 2020.

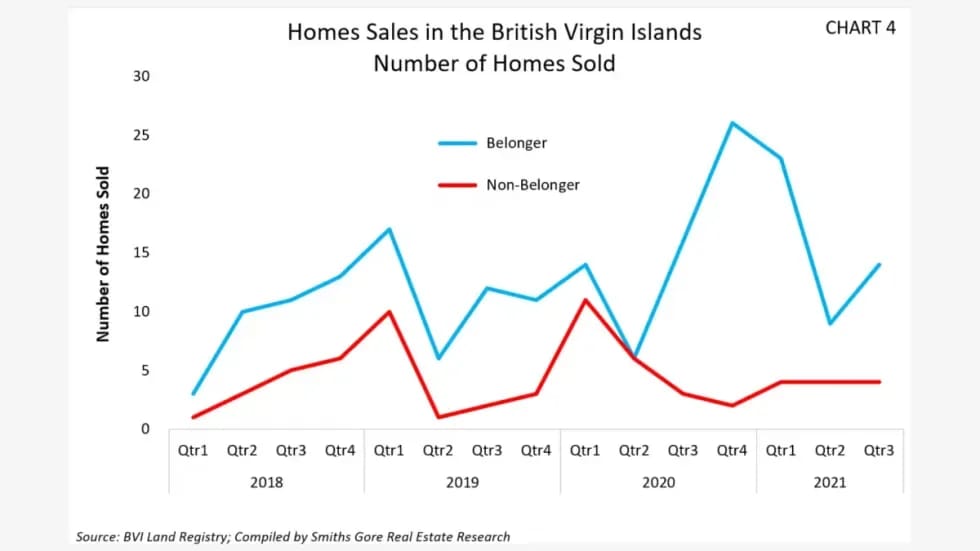

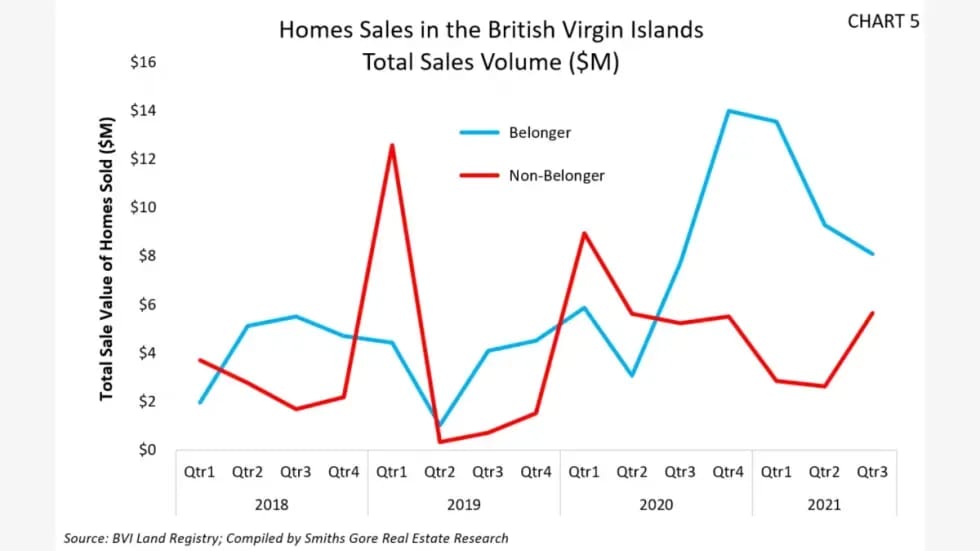

Charts 4 and 5 compare the number of homes sold to Belongers and Non-Belongers (Chart 4) between 2018 to 2021 (Q3) and the total sales volume for houses over the same period (Chart 5). The charts clearly show how house sales to Belonger investors have come to dominate the market in the BVI both in terms of number of sales and total sales volume.

There have been 271 house sales since 2018 with Belongers acquiring 205 which represents 76% of all house sales. The 271 sales equated to $156M in total sales volume with Belongers accounting for $94M in sales or 60% of the market in terms of value. Chart 4 also indicates how the sale of homes to Belongers peaked in late 2020 and early 2021 as Belonger purchasers took advantage of the stamp duty waiver. A similar peak occurs in Chart 5 representing the volume of sales to Belongers with the last quarter of 2020 and the first quarter of 2021 accounting for 30% of the total sale volume for the period 2018 to September 2021. Eighty percent of all house sales to Belongers were on Tortola accounting for $73M in total sales volume with an average home price on Tortola of $445,000 compared to $542,500 on Virgin Gorda.

There has been a total of 66 house sales to Non-Belongers between 2018 and September 2021 with 2020 representing the highest number of sales with 23 homes sold while the first three quarters of 2021 have seen a total of 16 sales to Non-Belongers. Of the 66 homes sold to Non-Belongers, 57% were on Tortola totaling $28.1M in sales volume at an average price of $740,000 compared to $1,415,000 on Virgin Gorda.

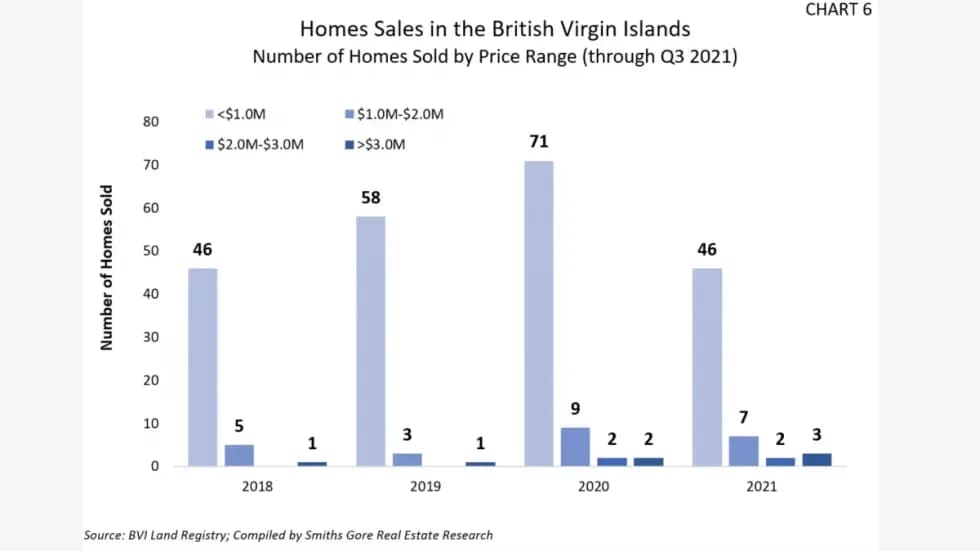

Chart 6 shows house sales between 2018 and September 2021 by price band. The data indicates that 87% of all house sales during this period are below $1.0M however this also includes the sale of damaged property in the years following Hurricane Irma which would have contributed to the number of sales below $1.0M. We estimate that approximately 23% of the sales below $1.0M were of hurricane damaged homes.

Chart 6 also shows that house sales over $1.0M accounted for only 13% of sales. There was a total of seven sales greater than $3.0M in this period of which three were at Oil Nut Bay. Two of the seven sales were to Belonger purchasers.

The market for land in the BVI has been active in the post Hurricane Irma landscape. Land acquisition has always been important to BV Islanders and even though many have “family land”, the ability to build a house, perhaps with an apartment beneath to assist with repaying the mortgage, is as much a part of life for BV Islanders as having a job. It is no surprise then that the land market has seen significant growth over the past few years, stimulated as well by the general movement of property post Irma, the stamp duty exemption for Belongers and the ability to obtain 100% loans on land. The land market has been particularly active on Tortola, assisted by the opening of a number of sub-divisions in different parts of the island.

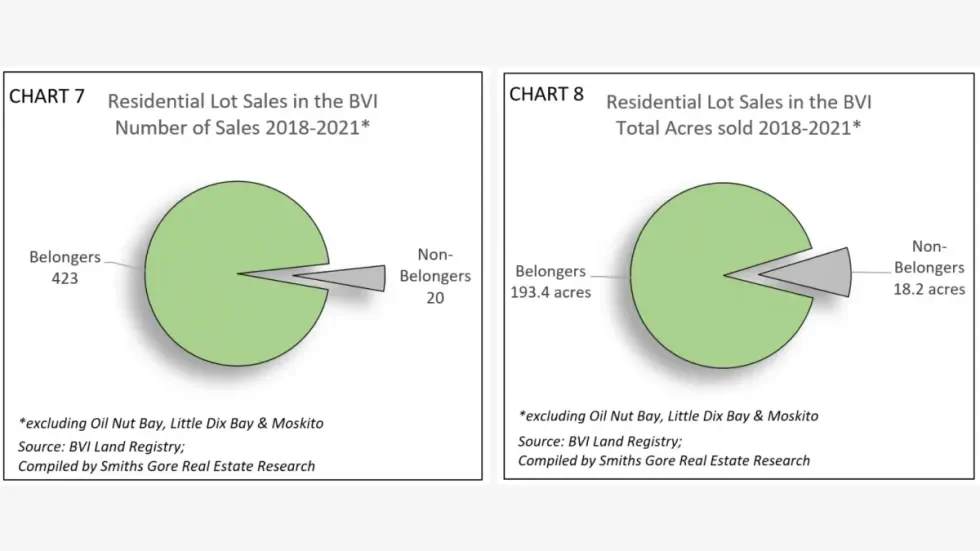

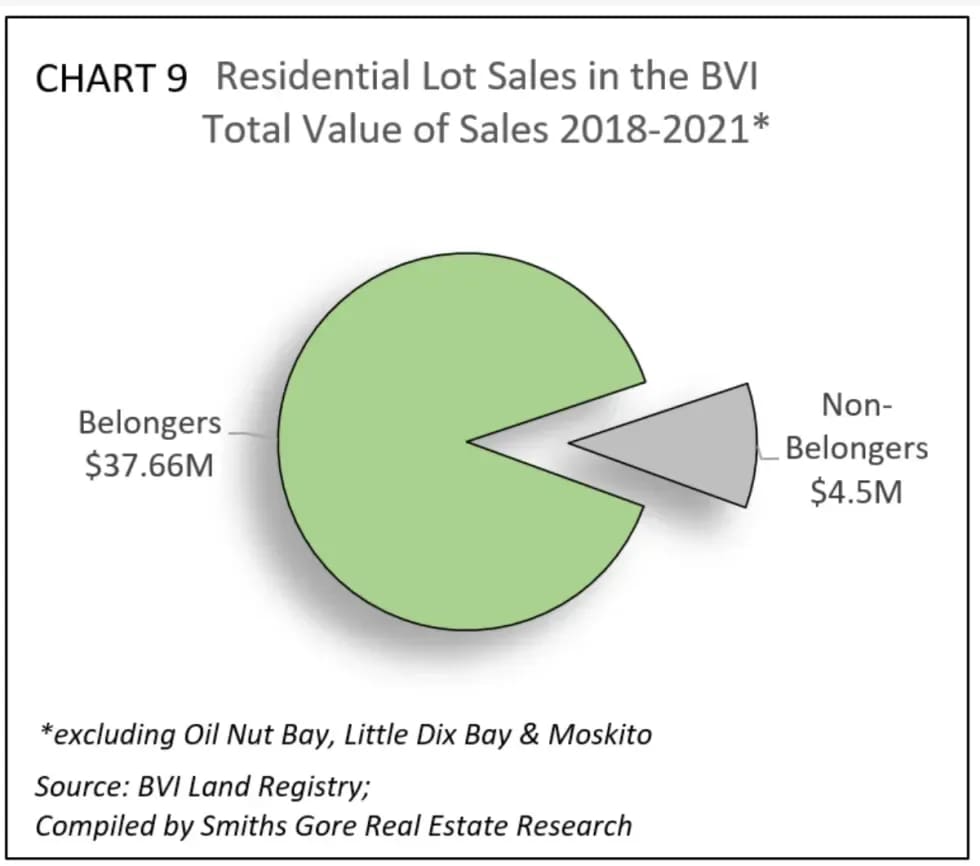

Charts 7, 8 and 9 breakdown the acquisition of the number of lots, acreage and total sales volume between Belongers and Non-Belongers for the period 2018 to September 2021 excluding Crown land and lots at the high-end residential sub-divisions at Oil Nut Bay, Little Dix Bay and Moskito Island.

There have been a total of 443 residential lot sales during this period with 423 lots being acquired by Belongers representing 95% of the residential lot market (Chart 6). Residential lots sales have accounted for the transfer of 211.6 acres (Chart 7) with sales to Belongers totaling 193.4 acres or 91% or the total acreage sold.

From this data, the average lot size sold to Belongers is 0.46 acre while the average lot size sold to Non-Belongers is 0.91 acre. In total, Belongers spent $37.7M acquiring lots over this time period (Chart 8) at an average price of $89,034 per transaction or $194,775 per acre. In contrast, Non-Belongers spent $4.5M on acquiring residential lots or $225,170 per transaction at an average of $246,775 per acre. There were a total of thirteen transactions within the high end residential sub-divisions at Oil Nut Bay, Little Dix Bay and Moskito Island representing a total of $43.5M in sales which equates to $3.35M per transaction or $2.32M per acre. Sales within these three developments represent 52% of total lot sales in the BVI.

Of the thirteen sales, three were to Belongers totaling $10.3M in sales or 24% of the total value of the lot sales within these developments.

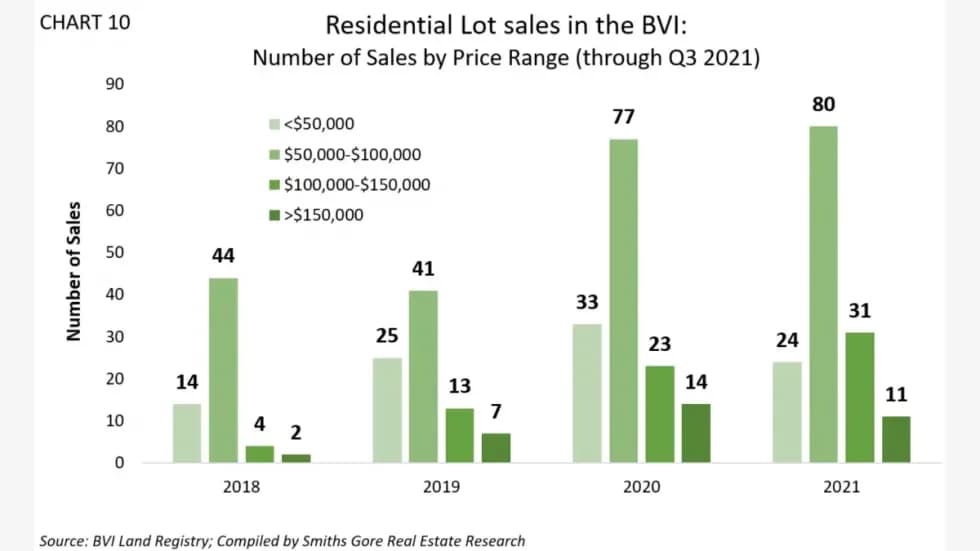

Outside of the three resort developments on Virgin Gorda (Oil Nut Bay, Moskito Island and Little Dix Bay), there have been a total of 443 lots sales between 2018 and September 2021. Chart 10 breaks down these lot sales into price bands, with 55% of lot sales falling between $50,000 to $100,000 and 22% under $50,000 leaving 23% of lots sales above $100,000.

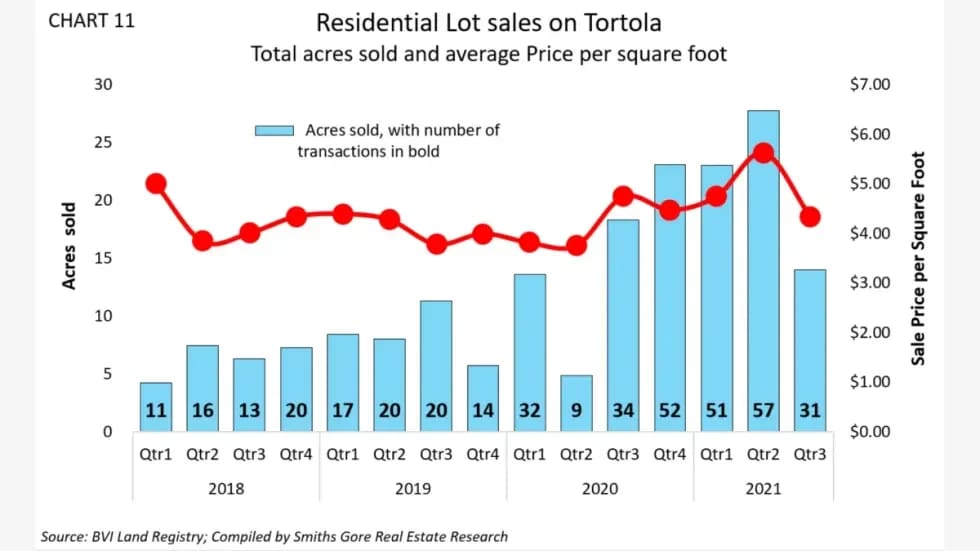

The market for residential lot sales is dominated by sales on Tortola, with the sales between 2018 and September 2021 reflected in Chart 11. The chart shows how the sale of residential lots increased substantially in the last two quarters of 2020 and first two of 2021 accounting for 49% of all residential lot sales on Tortola in this period.

Despite the increased demand, the average price for residential lots on Tortola has not changed significantly, showing a small increase at the end of 2020 in line with increased demand. The average price per square foot ranged between approximately $4.00 to $4.40 per square foot over this period.

One segment of the real estate transactions that is not captured by Land Registry data is the sale of property through the transfer of shares. Purchasers often acquire property in the BVI through a company and when selling, have the option of either selling the asset or selling the shares in the company. While the sale of an asset is recorded in Land Registry, the sale of shares in a company that owns real estate is not. Therefore, data relating to the sale of houses in the BVI does not reflect the sale of shares in a property company. In the past, the quantity of these transactions has been negligible, as most purchasers prefer not to take on the risk of buying shares in an existing company where warranties can be difficult to enforce. While there have been some sales of property through share transactions over the past three years, these have generally remained well in the minority.

As we move into 2022, the tourism sector is expecting a busy high season and already the islands feel different with the return of the cruise ships and anchorages once again looking full. With increased tourism will come the risk of more spikes in COVID cases. The BVI Government has been steering that difficult course finding the right balance between opening the economy, encouraging vaccination and implementing protocols to reduce and contain the risk of community spread of COVID.

The return of tourists will inevitably bring an increase in the number of foreign investors to the BVI seeking a house in the sun. While the substantial increase in Belonger investment in both land and houses since Hurricane Irma is excellent news, the more muted interest from foreign investors in the BVI at a time when other Caribbean islands are reporting a real estate boom highlights the movement of the real estate market in the BVI towards local investment. There has certainly been more interest from foreign investors in real estate in the BVI during 2021 but we may not see this impacting the sales data until late 2021 or early 2022 when sales to foreign investors eventually close.

The long road to reopening the economy through much of 2020 and 2021 will hopefully be behind us in 2022, with tourism looking set for a busy high season, provided the new variant Omicron does not spoil the fun. Its emergence at the end of the year has certainly caused consternation with new worldwide travel restrictions and economic impacts, but it remains too soon to know if this is just a scare or something more significant. We can also expect an increase in interest from foreign investors, as more people visit the BVI, and hopefully, the growth in investment from Belongers will continue after the end of the stamp duty waiver at the end of the year. The passing of the Investment Act and eventually the Business Licence Act will introduce a new environment for local and foreign investment alike. With policy surrounding these acts still to be announced, we will have to wait to see the impact these acts may have on investment and growth in the BVI.